Veterinary Orthopedic Implants Market Size, Trends and Insights By Product Type (Tibial Plateau Levelling Osteotomy (TPLO) Implants, Tibial Tuberosity Advancement (TTA) Implants, Total Knee Replacement Implants, Total Elbow Replacement (TER) Implants, Advanced Locking Plate System (ALPS), Others), By Application (Bone fractures, Elbow Dysplasia, Osteoarthritis, Patellar Luxation, Hip Dysplasia, Others), By End User (Veterinary Hospitals, Veterinary Clinics, Others), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | North America |

Major Players

- Narang Medical Limited

- Arthrex Vet Systems

- Integra LifeSciences

- BlueSAO

- Others

Reports Description

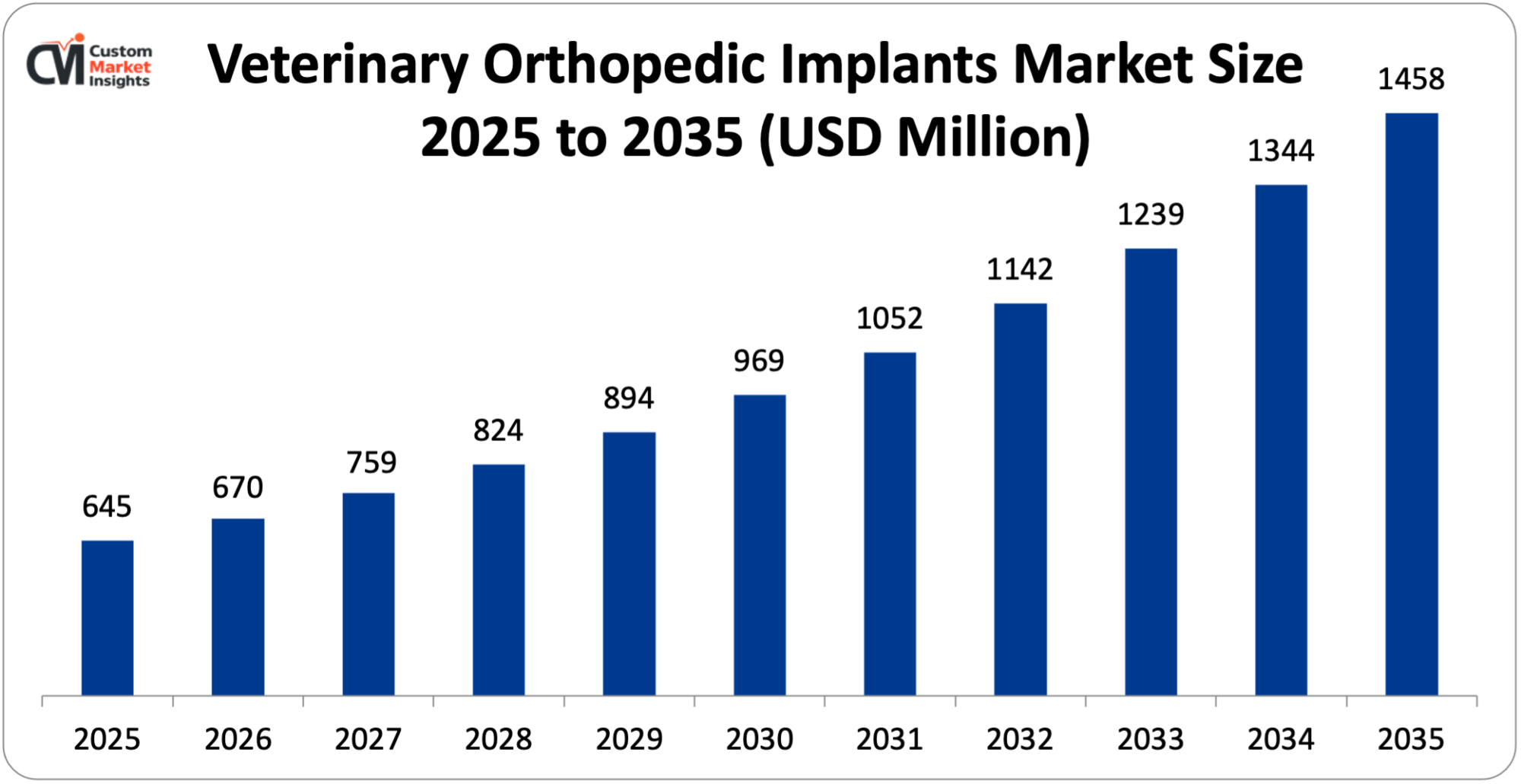

The market size of global veterinary orthopedic implants will be estimated at USD 645 million in 2025 and is expected to grow to between USD 670 million in 2026 and about USD 1458 million by 2035, with a current CAGR (compound annual growth rate) of 8.5% during the period of 2026 to 2035. Veterinary orthopedic implants are medical devices implanted into animals by veterinarians to treat, repair, or replace broken bones and joints from both small and large animals with problems such as fractures, deformities, ligament damage, or degenerative disease.

Veterinary orthopedic implants are made of biocompatible materials (such as stainless steel, titanium, or special alloys) and are used as plates, screws, pins, wires, or joint replacement devices. These implants are sometimes used during orthopedic surgery for pets, normally dogs and cats, but even larger animals, such as horses or farm animals, can be operated on with them. Veterinary orthopedic implants are used for mobility surgery to repair or replace broken joints or bones and treat diseased or broken animals.

Market Highlight

- In 2025, North America will dominate the global market with an estimated market share of 53%. The rising innovative product launch and the increasing pet ownership.

- The Asia Pacific is growing at the highest CAGR over the analysis period. The presence of major players drives the regional market.

- By product type, the total knee replacement implants are expected to hold a prominent market share over the projected period.

- By end user, the veterinary hospitals segment captures the largest market share in 2025.

Significant Growth Factors

The veterinary orthopedic implants market trends present significant growth opportunities due to several factors:

- Growing prevalence of orthopedic disorders in animals: The increased occurrence of animals with orthopedic disorders is one of the important trends driving the growth of the veterinary orthopedic implants market. This phenomenon is because conditions like fracture of bone, cranial cruciate ligament tears, hip dysplasia, arthritis, and joint deformities are quite prevalent among companion animals due to aging, rising obesity, hereditary congenital predispositions, and increased trauma or accidents. Due to these conditions affecting the normal functioning and structure of joints and bones, orthopedic implants, such as pins, screws, plates, joints, and replacements, are used.

- Increasing spending on animal healthcare: An important factor for the development of the market for veterinary orthopedic implants is the rise in expenditure on animal healthcare. In the current scenario, pet owners want to spend more money on advanced veterinary courses and treatment procedures to safeguard the health of their pet animals. The increase in disposable income, knowledge regarding animal health, and the rise in the trend of pet humanization have propelled the customers to opt for advanced medical procedures such as orthopedic surgeries. Also, structural innovations, an increasing number of pet insurance policies, and the creation of veterinary hospitals and specialty clinics are fueling the veterinary orthopedic implants market. For instance, according to the 2024-2025 National Pet Owners Survey by the American Pet Products Association (APPA), an estimated seventy-one percent of all households in the United States, or about 94 million families, have a pet. In 1988, only fifty-six percent of all American households had a pet—the first year the survey was taken. Total expenditures on the pet industry in the United States reached $152 billion in 2024—an increase of 3.4 percent from the total of $147 billion in 2023.

What are the Major Advances Changing the Veterinary Orthopedic Implants Market Today?

- 3D-printed and patient-specific implants: 3D-Printed and patient-specific implants will be a huge breakthrough in the veterinary orthopedic implants market. It will allow the design and manufacture of superior implants based on the relevant structure of the respective animal utilizing advanced imaging techniques, such as the CAT scan. The designer can have a prototype provided in the computer, enabling greater accuracy and fitting of the implants, leading to better results, better recovery, and reduced invasive surgery.

- Minimally invasive surgical techniques: Minimally invasive surgical techniques are revolutionizing the veterinary orthopedic implants market. Small incisions are used to do the procedures by using the special instruments also with the help of orthopedic imaging in order to reduce trauma of tissues in operation. Minimally invasive procedures enable veterinarians to implant orthopedic devices such as plates, screws, and pins more accurately and with less pain and blood loss than traditional interventions. This allows a speedy recovery, shorter hospital stays, and better surgical outcomes. As veterinary practices continue to employ new surgical technologies, minimally invasive surgery is becoming integral to orthopedic implant procedures, leading to improved patient outcomes and increased adoption of these techniques in veterinary medicine.

Category Wise Insights

By Product Type

Why Total Knee Replacement Implants Hold a Prominent Position in the Market?

The total knee replacement implants are expected to hold a prominent market share over the projected period. The main driving force for this segment to grow is attributed to the increasing incidences of various severe joint disorders such as osteoarthritis, ligament injuries, degenerative joint diseases, and others in pet animals (mainly dogs). As the age factor in pet animals increases, pet owners are willing to go for full surgical procedures like total knee replacement. Moreover, ever-increasing pet humanization and the surge in expenditure on customized veterinary services are motivating pet owners to choose complex orthopedic procedures that help animals regain mobility and lead a better life. Additionally, these continuous advances in prosthetic designs and materials have also contributed to an increased acceptance of total knee replacement implants and, therefore, to increased revenue for veterinary practices and enhanced life quality for pet animals in this context.

The Total Elbow Replacement (TER) Implants segment is expected to grow at a rapid rate during the analysis period. The increase in total elbow replacement procedures recently is mostly associated with increased incidence of elbow dysplasia, severe arthritis, and traumatic joint injuries in pets, especially in large dog breeds. This accounts for chronic pain and incapacity and, therefore, makes total elbow replacement an attractive surgical option. Increasing awareness among consumer pet owners of newer veterinary orthopedic procedures and increasing availability of veterinary orthopedic surgeons is also boosting the revenue growth for this segment. Innovation in the design of the implants, improved biocompatible materials, and advanced surgical techniques are improving the treatment results, which in turn motivates the practice of total elbow replacement procedures.

By End User

Why Veterinary Hospitals Dominates the Veterinary Orthopedic Implants Market?

The veterinary hospitals segment captures the largest market share in 2025. Veterinary hospitals have all the latest equipment and experienced Veterinarians and this attracts the animal owners to bring their animals to veterinary hospitals for better and effective treatment. In addition, the larger veterinary hospitals have enough funds to purchase the latest equipment, which can decrease the time taken for procedures and make them pain-free for small animals. All these factors make the veterinary hospitals very popular.

The veterinary clinics segment is growing at a rapid rate. The uptrend in this segment is fueled by the proliferation of veterinary clinics offering the most modern diagnostic and surgical services for the management of companion animals. Many clinics are importing the latest imaging systems as well as sophisticated orthopedic surgical equipment that has enabled surgeons to operate upon their patients for complicated cases such as ligament reconstruction, joint transplantation, and fracture repair. Furthermore, increasing in-clinic visits by pets arising from injuries, age-related bone abnormalities, and orthopedic conditions induced by obesity are expected to foster demand for orthopedic implants such as plates, screws, and pins. Increasing pet ownership and expenditure on animal health are likely to encourage owners to seek orthopedic treatment for animals in veterinary clinics.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 670 million |

| Projected Market Size in 2035 | USD 1458 million |

| Market Size in 2025 | USD 645 million |

| CAGR Growth Rate | 8.5% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Product Type, Application, End User and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is North America Veterinary Orthopedic Implants Market Size?

Its market size, in terms of North America veterinary orthopedic implants, is projected to be USD 342 million in 2025 with a growth of about USD 704 million in 2035 with a CAGR of 7.5% between 2026 and 2035.

Why did North America Dominate the Veterinary Orthopedic Implants Market in 2025?

In 2025, North America will dominate the global market with an estimated market share of 53%. This growth is mainly attributed to the rising rate of pet ownership and the thriving pet humanization trend not only in North America but also throughout the rest of the region. Veterinary customers in North America are willing to invest more in their pets’ treatment and rehabilitation, especially in the form of advanced veterinary procedures, such as complex orthopedic surgeries where implants are involved, such as plates, screws, and joint replacement systems, among others. This trend is partly ascribed to the large and sophisticated local veterinary medicare system along with a considerable number of specialized veterinary hospitals. The combination of the major market presence of the most renowned veterinary medical device manufacturer in the region, the rising pet insurance coverage, increased pet awareness, and greater attentiveness to animal healthcare has led to an annual increase in veterinary orthopedic implants.

US Veterinary Orthopedic Implants Market Trends

In the North American region, the US leads the industry expansion over the projected period. The increasing pet ownership is one of the significant factors driving the market growth. For instance, according to the American Veterinary Medical Association, in 2025, approximately 43% of US households will own a dog. Further, the rising animal healthcare expenditure propels the market growth.

Why is Europe Experiencing a Significant Growth in the Veterinary Orthopedic Implants Market?

Europe holds a significant market share. Regional growth in Europe is attributed to the surge in pet population and awareness of sophisticated animal healthcare. The trendy pet monogamous trend among the European countries such as the United Kingdom, Germany, and France has facilitated the pet owners getting specialized veterinary treatments and surgeries like orthopedic surgeries. Moreover, the presence of an established veterinary healthcare network comprising several veterinary clinics, referral hospitals, and skilled orthopedic surgeons is helping the market in revenue generation.

Growing number of bone fractures, joint disorders, and ligament problems in domestic animals is projected to attract a large number of customers seeking implants like plates, screws, and joint replacements, thereby raising revenues. Motivating animal welfare legislations and expanding pet insurance also are factors boosting the market share for advanced veterinary orthopedic procedures.

UK Veterinary Orthopedic Implants Market Trends

The UK held the dominant position in the market. This growth can also be attributed to a growth in the pet population along with an awareness of more advanced veterinary treatments. A pronounced culture of pet ownership and pet humanization has led pet owners to pursue more specialized care for orthopedic conditions, including fractures, ligament trauma, degenerative joint disease, and others.

Why is the Asia Pacific is growing at a rapid rate in the Veterinary Orthopedic Implants Market?

The Asia Pacific is expected to grow at a rapid rate over the projected period. The market growth has been driven by the exponential growth in pet ownership and increase in awareness of the health needs of animals. Increasing disposable incomes and urbanization in countries like Japan, China, India, and Australia are tempting pet owners to spend significantly on more advanced animal treatments like orthopedic operations.

The ever-growing presence of veterinary hospitals/clinics coupled with the availability of state-of-the-art diagnostic and surgical facilities is further enabling the demand for orthopedic implants. The rising number of animal fractures and joint and ligament injuries is further accentuating the need for orthopedic implants like joint replacement systems, plates, and screws.

India Veterinary Orthopedic Implants Market Trends

India led the Asia Pacific market. An increase in pet ownership, heightened awareness of pet health care, and rising pet-related spending fuel this growth. Increase in the number of veterinary clinics, increasing middle-class income, and the adoption of modern implant technologies, as well as government programs to support animal welfare, are contributing to the country’s market demand for veterinary orthopedic implants.

Why is the Middle East & Africa Region is growing rapidly in the Veterinary Orthopedic Implants?

The MEA region is growing at a steady rate over the projected period. The increase has been attributed to increasing awareness about animal healthcare and the number of companion animals. As urbanization is increasing and the economic conditions are improving in various Middle Eastern countries, the pet owners are now looking forward to better treatments such as orthopedic surgery for fracture and joint disorders.

UAE Veterinary Orthopedic Implants Market Trends

UAE is growing at the highest CAGR during the forecast period. The increase in animal healthcare expenditure in the area drives the market growth.

Top Players in the Veterinary Orthopedic Implants Market and Their Offerings

- Narang Medical Limited

- Arthrex Vet Systems

- Integra LifeSciences

- BlueSAO

- DePuy Synthes (Johnson & Johnson)

- Fusion Implants

- GerVetUSA

- GPC Medical Ltd.

- Braun

- Movora (Vimian Group)

- AmerisourceBergen Corporation (Cencora Inc.)

- Ortho Max

- Orthomed

- Rita Leibinger

- Veterinary Instrumentation

- Others

Key Developments

Veterinary orthopedic implants market has experienced considerable changes in the last two years as the market players are trying to diversify their technological aspects and develop product portfolios using strategic approaches.

- In July 2025, Movora, a global leading provider of veterinary orthopedic solutions, and the AO Foundation, a global leader in medical education and innovation, have signed a Memorandum of Understanding (MoU) to collaborate on advancing veterinary education beginning in 2026. Through this partnership, Movora will support a series of AO-led educational events across North America, Western Europe, and Japan. These courses-delivered independently by the AO-will focus on surgical principles and hands-on skills development in veterinary orthopedics. While the AO retains full control over course design and delivery, Movora will provide logistical and technical support, including workstations, equipment, and on-site personnel. (https://www.newsfilecorp.com/release/259145/Movora-and-AO-Foundation-Enter-Strategic-Collaboration-to-Advance-Veterinary-Education)

- In March 2026, Synchrocare, LLC, a U.S. medical device distributor founded in 2005, announced a new strategic distribution partnership with BioPoly, an orthopedic biomaterials company focused on polymer-based implant solutions. Under the agreement, Synchrocare will distribute BioPoly’s products nationwide, expanding surgeons’ access to implant technology designed to provide strength, durability, and long-term biocompatibility. (https://www.clarionledger.com/press-release/story/121423/synchrocare-and-biopoly-form-strategic-distribution-partnership-to-expand-access-to-advanced-polymer-implant-technology/)

These strategic measures have enabled the companies to reinforce their competitive positions, increase the product line, boost their technological competencies, and also seize growth opportunities in the fast-growing Veterinary Orthopedic Implants market.

The Veterinary Orthopedic Implants Market is segmented as follows:

By Product Type

- Tibial Plateau Levelling Osteotomy (TPLO) Implants

- Tibial Tuberosity Advancement (TTA) Implants

- Total Knee Replacement Implants

- Total Elbow Replacement (TER) Implants

- Advanced Locking Plate System (ALPS)

- Others

By Application

- Bone fractures

- Elbow Dysplasia

- Osteoarthritis

- Patellar Luxation

- Hip Dysplasia

- Others

By End User

- Veterinary Hospitals

- Veterinary Clinics

- Others

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Veterinary Orthopedic Implants by Segments

- 2.1.2. Veterinary Orthopedic Implants by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Veterinary Orthopedic Implants Market Attractiveness Analysis, By Product Type

- 2.2.3. Veterinary Orthopedic Implants Market Attractiveness Analysis, By Application

- 2.2.4. Veterinary Orthopedic Implants Market Attractiveness Analysis, By End User

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Growing prevalence of orthopedic disorders in animals

- 3.1.2. Increasing spending on animal healthcare

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter’s Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Veterinary Orthopedic Implants Market – By Product Type

- 4.1. Product Type Market Overview, By Product Type Segment

- 4.1.1. Veterinary Orthopedic Implants Market Revenue Share, By Product Type, 2025 & 2035

- 4.1.2. Tibial Plateau Levelling Osteotomy (TPLO) Implants

- 4.1.3. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Tibial Tuberosity Advancement TTA Implants

- 4.1.7. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Total Knee Replacement Implants

- 4.1.11. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Total Elbow Replacement (TER) Implants

- 4.1.15. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Advanced Locking Plate System (ALPS)

- 4.1.19. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Others

- 4.1.23. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Product Type Market Overview, By Product Type Segment

- Chapter 5. Veterinary Orthopedic Implants Market – By Application

- 5.1. Application Market Overview, By Application Segment

- 5.1.1. Veterinary Orthopedic Implants Market Revenue Share, By Application, 2025 & 2035

- 5.1.2. Bone fractures

- 5.1.3. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Elbow Dysplasia

- 5.1.7. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Osteoarthritis

- 5.1.11. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Patellar Luxation

- 5.1.15. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Hip Dysplasia

- 5.1.19. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Others

- 5.1.23. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Application Market Overview, By Application Segment

- Chapter 6. Veterinary Orthopedic Implants Market – By End User

- 6.1. End User Market Overview, By End User Segment

- 6.1.1. Veterinary Orthopedic Implants Market Revenue Share, By End User, 2025 & 2035

- 6.1.2. Veterinary Hospitals

- 6.1.3. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Veterinary Clinics

- 6.1.7. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Others

- 6.1.11. Veterinary Orthopedic Implants Share Forecast, By Region (USD Million)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1. End User Market Overview, By End User Segment

- Chapter 7. Veterinary Orthopedic Implants Market – Regional Analysis

- 7.1. Veterinary Orthopedic Implants Market Overview, By Region Segment

- 7.1.1. Global Veterinary Orthopedic Implants Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global Veterinary Orthopedic Implants Market Revenue, By Region, 2026 – 2035 (USD Million)

- 7.1.3. Global Veterinary Orthopedic Implants Market Revenue, By Product Type, 2026 – 2035

- 7.1.4. Global Veterinary Orthopedic Implants Market Revenue, By Application, 2026 – 2035

- 7.1.5. Global Veterinary Orthopedic Implants Market Revenue, By End User, 2026 – 2035

- 7.2. North America

- 7.2.1. North America Veterinary Orthopedic Implants Market Revenue, By Country, 2026 – 2035 (USD Million)

- 7.2.2. North America Veterinary Orthopedic Implants Market Revenue, By Product Type, 2026 – 2035

- 7.2.3. North America Veterinary Orthopedic Implants Market Revenue, By Application, 2026 – 2035

- 7.2.4. North America Veterinary Orthopedic Implants Market Revenue, By End User, 2026 – 2035

- 7.2.5. U.S. Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.2.6. Canada Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.2.7. Mexico Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.2.8. Rest of North America Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.3. Europe

- 7.3.1. Europe Veterinary Orthopedic Implants Market Revenue, By Country, 2026 – 2035 (USD Million)

- 7.3.2. Europe Veterinary Orthopedic Implants Market Revenue, By Product Type, 2026 – 2035

- 7.3.3. Europe Veterinary Orthopedic Implants Market Revenue, By Application, 2026 – 2035

- 7.3.4. Europe Veterinary Orthopedic Implants Market Revenue, By End User, 2026 – 2035

- 7.3.5. Germany Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.3.6. France Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.3.7. U.K. Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.3.8. Russia Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.3.9. Italy Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.3.10. Spain Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.3.11. Netherlands Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.3.12. Rest of Europe Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific Veterinary Orthopedic Implants Market Revenue, By Country, 2026 – 2035 (USD Million)

- 7.4.2. Asia Pacific Veterinary Orthopedic Implants Market Revenue, By Product Type, 2026 – 2035

- 7.4.3. Asia Pacific Veterinary Orthopedic Implants Market Revenue, By Application, 2026 – 2035

- 7.4.4. Asia Pacific Veterinary Orthopedic Implants Market Revenue, By End User, 2026 – 2035

- 7.4.5. China Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.4.6. Japan Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.4.7. India Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.4.8. New Zealand Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.4.9. Australia Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.4.10. South Korea Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.4.11. Taiwan Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.4.12. Rest of Asia Pacific Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.5. The Middle-East and Africa

- 7.5.1. The Middle-East and Africa Veterinary Orthopedic Implants Market Revenue, By Country, 2026 – 2035 (USD Million)

- 7.5.2. The Middle-East and Africa Veterinary Orthopedic Implants Market Revenue, By Product Type, 2026 – 2035

- 7.5.3. The Middle-East and Africa Veterinary Orthopedic Implants Market Revenue, By Application, 2026 – 2035

- 7.5.4. The Middle-East and Africa Veterinary Orthopedic Implants Market Revenue, By End User, 2026 – 2035

- 7.5.5. Saudi Arabia Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.5.6. UAE Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.5.7. Egypt Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.5.8. Kuwait Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.5.9. South Africa Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.5.10. Rest of the Middle East & Africa Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.6. Latin America

- 7.6.1. Latin America Veterinary Orthopedic Implants Market Revenue, By Country, 2026 – 2035 (USD Million)

- 7.6.2. Latin America Veterinary Orthopedic Implants Market Revenue, By Product Type, 2026 – 2035

- 7.6.3. Latin America Veterinary Orthopedic Implants Market Revenue, By Application, 2026 – 2035

- 7.6.4. Latin America Veterinary Orthopedic Implants Market Revenue, By End User, 2026 – 2035

- 7.6.5. Brazil Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.6.6. Argentina Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.6.7. Rest of Latin America Veterinary Orthopedic Implants Market Revenue, 2026 – 2035 (USD Million)

- 7.1. Veterinary Orthopedic Implants Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global Veterinary Orthopedic Implants Market: Company Market Share, 2025

- 8.2. Global Veterinary Orthopedic Implants Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. Narang Medical Limited

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. Arthrex Vet Systems

- 9.3. Integra LifeSciences

- 9.4. BlueSAO

- 9.5. DePuy Synthes (Johnson & Johnson)

- 9.6. Fusion Implants

- 9.7. GerVet

- 9.8. GPC Medical Ltd.

- 9.9. B. Braun

- 9.10. Movora (Vimian Group)

- 9.11. AmerisourceBergen Corporation (Cencora Inc.)

- 9.12. Ortho Max

- 9.13. Orthomed

- 9.14. Rita Leibinger

- 9.15. Veterinary Instrumentation

- 9.16. Others.

- 9.1. Narang Medical Limited

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Custom Market Insights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

List Of Figures

Figures No 1 to 31

List Of Tables

Tables No 1 to 46

Prominent Player

FAQs

The key players in the market are Narang Medical Limited, Arthrex Vet Systems, Integra LifeSciences, BlueSAO, DePuy Synthes (Johnson & Johnson), Fusion Implants, GerVetUSA, GPC Medical Ltd., B. Braun, Movora (Vimian Group), AmerisourceBergen Corporation (Cencora Inc.), Ortho Max, Orthomed, Rita Leibinger, Veterinary Instrumentation, Others.

Government legislation plays an important role in shaping the veterinary orthopedic implants industry in its entirety, as the industry‘s intentions towards maintaining a high and uniform level of safety and quality and efficiency of veterinary medical appliances are reinforced with requirements for the manufacture and testing of Veterinary orthopedic implants that are enforced prior to approval of their application on an animal, thereby inviting acceptance of the welfare of animals and credibility of the veterinary practices. Animal welfare legislation and guidelines for veterinary surgeons have partly helped the manufacturers to bring about innovation and can be a driving force for new surgical procedures to be introduced (e.g., minimally invasive procedures); they can, however, result in regulation of a company’s product development, with higher requirements for approvals.

Pricing will have a significant influence on the market for veterinary orthopedic implants. High prices for orthopedic implants and surgeries may inhibit adoption to a significant degree, in particular in emerging markets, where pet owners may be less willing to pay for expensive procedures. Conversely, pet ownership in developed economies benefits from high disposable incomes, pet insurance, and a willingness of owners to spend more on their pets, thus helping to balance out the issue of affordability. As veterinary orthopedic implant manufacture becomes more efficient and veterinary orthopedic surgery becomes more affordable, this issue should become less prominent.

According to the present analysis and forecast modeling, the market of veterinary orthopedic implants will witness a significant growth of about USD 1458 million in the year 2035 with the growing pet humanization trend, increased investment in advanced healthcare technology, and increasing collaboration with a CAGR of 8.5% between the years 2026 and 2035.

It is projected that North America will hold the largest market share in the veterinary orthopedic implants market in the forecast period, with a share of about 53% of the global market share, which is attributed to the presence of major players and increasing animal healthcare expenditure.

The Asia Pacific is expected to grow at the highest CAGR during the forecast period. The growth in the region is owing to the rising disposable income and increasing pet ownership.

The veterinary orthopedic implants market growth is primarily driven by increasing pet ownership and the pet humanization trend. Pet humanization trend leads the pet owners to be more willing to invest in advanced veterinary procedures.