Peer to Peer P2P Lending Market Size, Trends and Insights By Lending Type (Consumer Lending (Personal Loans, Debt Consolidation, Medical, Home Improvement), Business Lending (SME Working Capital, Invoice Financing, Trade Finance, Equipment), Real Estate Lending (Residential, Commercial, Bridge Loans, Development Finance), Student Loan Refinancing, Agricultural Lending, Other Lending Types (Auto, Green Finance, Microloans)), By End-User (Individual Borrowers (Employed Individuals, Self-Employed, Gig Economy Workers), Small & Medium Enterprises (Micro, Small, Medium Businesses), Real Estate Developers, Agricultural Borrowers, Other End-Users (Non-Profits, Government-Linked Entities)), By Business Model (Marketplace/Platform Model (Investor-Funded, Originate-to-Distribute), Balance Sheet Model (Platform Retains Loan Exposure), Hybrid Model (Mixed Funding and Retention), Other Business Models (Notary Model, Guaranteed Return Models)), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- LendingClub Corporation

- Prosper Marketplace Inc.

- Funding Circle Holdings plc

- Zopa Bank Ltd.

- Others

Reports Description

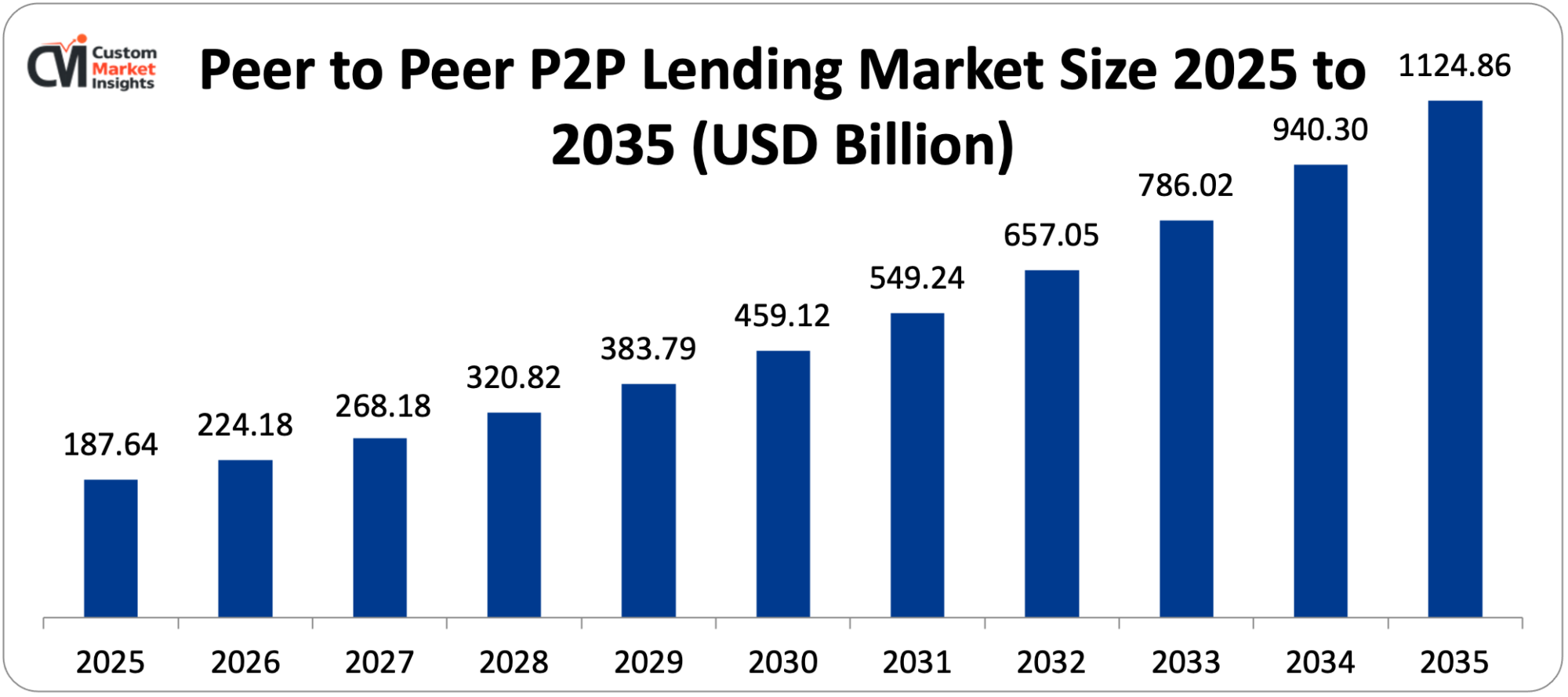

The worldwide peer-to-peer (P2P) lending market is estimated to be worth USD 187.64 billion in the year 2025. Expected growth is steep: The market is expected to grow to reach USD 224.18 billion in 2026 and to reach around USD 1,124.86 billion by 2035 and will grow at a 17.5% compound annual growth rate (CAGR) between 2026 and 2035. This expansion is attributed to a global movement for financial inclusion driving the expansion of alternative credit, which is a pressing demand for credit among underbanked and underserved populations excluded from the financial system by traditional banks. Digital lending platforms allow free loop origination, credit evaluation, and fund payback, which bring transaction costs lower than those of traditional banking. Finally, institutional investors are coming online to the P2P platforms as an alternative asset class, looking for risk-adjusted returns that will beat comparable fixed-income investments in low interest rate environments, regulatory frameworks in major economies are maturing in which the legal status of the P2P lending industry is formalised and compliance infrastructure needed for broader participation in the industry is built. At the same time, artificial intelligence and machine learning are revolutionizing the assessment of credit risk, replacing traditional underwriting models based on credit bureau data with behavioral, transactional and alternative data scoring models. These new models are more precise on credit worthiness on the whole population of borrowers. As a combination, these developments promote long-run, outstanding market growth during the period in question.

Market Highlight

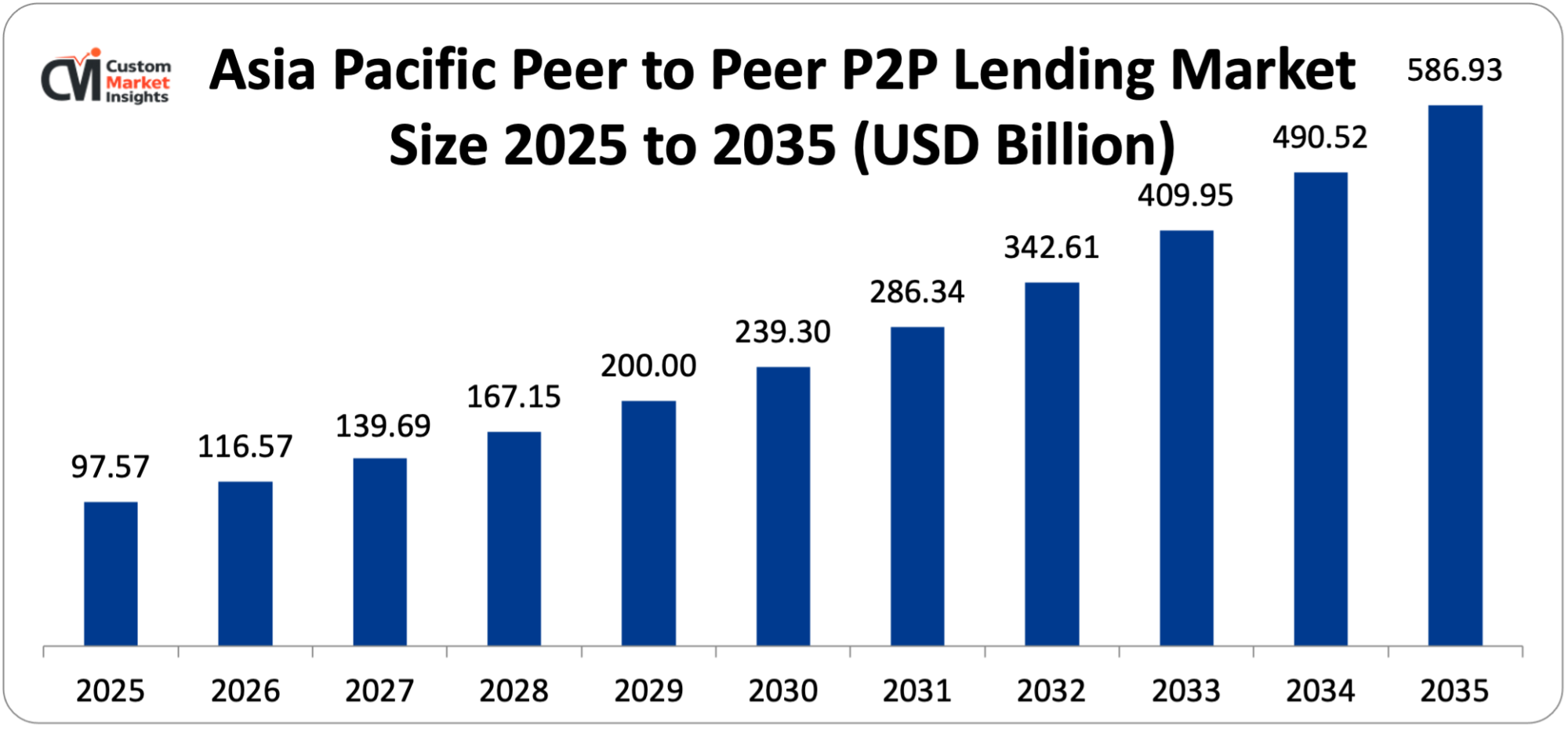

- Growing P2P lending market Asia Pacific dominated the peer to peer P2P lending market with a market share of 52% in 2025.

- The North American market is projected to grow at a CAGR of 16.8% during 2026-2035.

- The market share for the consumer lending segment is about 44% in the year 2025.

- By the type of lending, the business lending segment is experiencing the fastest CAGR of 19.4% during the period 2026-2035.

- By end-user, the individual borrowers segment accounted for the largest market share of 48% in 2025, whereas the small & medium enterprises segment is projected to grow at the fastest CAGR rate of 20.6% over the projected period between 2026 and 2035.

- By business model, the marketplace/platform model was the largest contributor to market share of 68% in 2025, while the marketplace model also grew the fastest at 18.2% compound annual growth rate (CAGR) from 2026 to 2035.

Significant Growth Factors

The Peer to Peer P2P Lending Market Trends present significant growth opportunities due to several factors:

- Financial Inclusion Imperative and Credit Access Gap Driving P2P Platform Adoption: The World Bank estimates that roughly 1.4 billion adults around the world still do not have a bank account, and hundreds of millions more are underbanked (they have basic bank accounts but are unable to access affordable credit). Traditional credit scoring models have difficulty scoring borrowers with thin, non-traditional or non-existent credit histories. This creates demand for P2P lending platforms that employ alternative data and technology enabled lending economics to serve borrowers that banks systematically exclude or underserve. Conventional bank underwriting is based on credit bureau ratings, collaterals, income paper trails and loan history, which bars major blocks of the adult population: self-employed individuals whose sources of income are not equal to those verified by conventional employment; new borrowers suffer shortfeings in these credit scores; proprietors with small enterprises, and those in the rural or informal sector, whose verifiable income is not documented. Alternative data used in P2P is mobile phone usage history, social media usage, e-commerce transaction history, utility payment history, education qualification, and behavioral biometric to complement or substitute the traditional bureau data. This approach delivers credit approval rates of 60-80% for applicants that would otherwise be rejected by banks while keeping default rates acceptable due to the predictive accuracy of alternative data models that are validated against large historical data sets. The need to broaden credit access to the underbanked through the use of technology based financial services has been studied by the McKinsey Global Institute which indicates the potential addition of USD 3.7 trillion to the GDP in emerging markets, which provides valuable economic incentive to P2P lending. The Covid-19 pandemic underscored the importance of digital lending, as the P2P platforms survived the pandemic and offered emergency credit options and loan applications without any physical contact, due to the closing of bank branches, accelerating awareness among the borrowers and keeping the rate of adoption high even after the pandemic.

- Small Business Credit Gap and SME Finance Innovation Driving Business P2P Adoption: The small business credit gap around the world is considerable. The International Finance Corporation estimates USD 5.2 trillion per year financing gap in the formal financial system for SMEs in the developing economy in particular, where bank credit to SMEs is a fraction of productive credit demand. This gap is the biggest addressable opportunity in the P2P lending market because the credit needs of SME borrowers are large and have high economic returns, which creates employment and GDP growth. Traditional bank SME lending economics are unprofitable with small loan values (fixed costs of assessment, documentation review and monitoring dominating interest income) with thresholds of USD 100 000 – USD 500 000 in developed markets, and similar levels in developing economies. And many creditworthy SMEs with loan requirements less than these thresholds are excluded from bank credit at any price. P2P business lending platforms can automate assessment using API connected accounting software, real time analysis of transactions, tax record review, and alternative data to get assessment cost of USD 100 – USD 500 per application compared to USD 2000 – USD 10,000 for manual underwriting by banks. This allows profitable lending at loan values of USD 5000 – USD 250 000 that traditional banks would find unattractive. The SME platform value proposition consists of 24-48 hour credit decisions (versus 4-12 weeks), digital documentation (versus visiting a branch), flexible loan structures in line with cash flow patterns, and transparent pricing (versus hidden fees). These customer experience benefits drive adoption by SMEs outside of pure interest rate comparisons (research shows consistently that SMEs are willing to pay modest rate premiums for the speed, convenience and certainty that P2P platforms offer compared to bank SME lending).

What are the Major Advances Changing the Peer to Peer P2P Lending Market Today?

- Artificial Intelligence and Alternative Data Credit Scoring Transformation: The wholesale transformation of P2P platform credit underwriting no longer being based on conventional credit bureau score-dependent pricing to artificial intelligence and machine learning models that used hundreds of alternative data variables – such as real-time banking transaction patterns, mobile usage data, e-commerce purchase behavior, social connection quality, employment verification through payroll API connections, rental payment histories, and utility payment records – is at once, both improving the predictive accuracy of credit risk models to better than what can be obtained using bureau score-dependent pricing, and creating a sustainable competitive advantage to those platforms that has acquired the proprietary data assets and model training Machine learning credit models recognise non-linear interactions between credit risk predictors not reflected in linear credit scoring models, capturing the non-linear patterns in other data that differentiate creditworthy and high-risk borrowers within the population that is classified homogeneously as subprime or unsolvable by conventional bureau score models. The published results of its machine learning credit models by LendingClub, which showed that AI-enhanced underwriting decreases charge-off rates by 1520% to the same borrower interest rate levels as bureau score-based underwriting and provides credit approval to 2030% more applicants, represent a reference quantification of the financial value of AI credit model superiority that drives investment in credit model sophistication on the platform. The open banking regulatory efforts such as the Open Banking Standard in the UK, the Payment Services Directive 2 of the European Union which allows account information service access, and analogous consumer data portability schemes in Australia, Singapore, and, to a growing extent, the United States are establishing regulatory frameworks that allow P2P platforms to obtain access to bank transaction data of borrowers as they seek to grant them real-time cash flow and behavioral data which dramatically improves the accuracy of credit assessment among self-employed and gig economy workers with complex income patterns that nonetheless are well-represented in the bank transaction data The Account Aggregator system of India – which started functioning in 2021 and continues to expand to millions of active users sharing their financial data with lending platforms – is the most sophisticated public digital financial infrastructure in the world to support the evaluation of credit using alternative data, and P2P networks on the AA platform achieve credit inclusion of previously unserved borrowers whose creditworthiness was previously unknown to the conventional bureau scoring system.

- Institutional Investor Integration and Secondary Market Development: Institutional Investor Integration and Secondary Market Development: The increased involvement of institutional investors, such as hedge funds, family offices, asset managers, insurance companies, and bank treasury functions, as lenders to P2P lending platforms is radically altering the capital structure of the P2P industry as originally designed, with individual investor-based P2P lenders, to one of a more institutional capital-backed marketplace with large-volume institutions as key funding providers and retail investor-based P2P lenders as key end The P2P platform lending has been adopted by the institutional investor as an alternative fixed income asset category because of its historically high risk-adjusted returns, when compared to a similarly rated corporate bond, its short duration and monthly cash flow form providing liquidity benefits over long-dated fixed income instruments, and its low correlation with the movements of the asset prices in the public markets, giving it portfolio diversification benefits; this has dramatically changed the lending capacity of the major platforms against the retail investor fundraising constraint which previously limited the origination volume, into the institutional capital provision that enables rapid scale-up of origination The shift of P2P lenders to institutional funding domination, with institutional buyers constituting half or more of the loan funding on established and large platforms, by LendingClub, Prosper, and Funding Circle, shows the commercial validation of P2P lending as an institutional asset class, although this shift has spawned regulatory and philosophical debate on whether institutional dominated P2P platforms have retained their original peer-to-peer nature or have become a different kind of technology enabled alternative credit fund. Development of Secondary market — allowing investors to trade existing P2P loan portfolios prior to maturity, allowing liquidity to investors with dynamic investment needs and allowing the P2P loan credit risk to be discovered in liquidity, previously unavailable to institutional investors whose process of managing their portfolios needed liquidity that the prior buy-and-hold loan maturity model could not offer. The securitization of P2P loans – where digital asset infrastructure based on blockchains allows the fractionalization and secondary trading of loan interest with automatic settlement and performance monitoring.

- Embedded Finance and Platform Integration Expanding P2P Reach: Embedded Finance and Platform Integsts under those that can be effected via traditional loan tradinration Expanding P2P Reach: The progressive integration of P2P lending capabilities with non-financial digital platforms – such as e-commerce marketplaces, accounting software, supply chain management systems, payroll systems, and point-of-sale systems – via embedded finance application programming interfaces is growing P2P access to credit by borrowers at the moment of commercial need without them having to take the initiative to seek out a lending platform, significantly lowering the cost of customer acquisition The Alibaba Ant Financial service of lending to Alibaba marketplace sellers on the basis of their history of transaction into the Alibaba ecosystem is the most commercially successful application of embedded P2P-style lending, proving that platform transaction history can be used to evaluate credit worthiness better than traditional bureau-based underwriting of merchants whose creditworthiness is directly observable as a result of their business performance on the platform. The buy now pay later innovation, where temporary embedded payment credit offered at the point of sale to merchants has shown consumers adopt it in huge numbers and gradually being extended into longer term consumer credit offerings, is a model of embedded finance that creates competitive pressure on the existing P2P consumer lending business models as well as confirming the consumer desire to access frictionless digital credit as pioneered by P2P consumer lending platforms. Xero and QuickBooks accounting software integration with P2P business lending platforms – allowing automatic credit evaluation based on accounting data already in the borrower accounting system, and a pre-qualified credit offer generated directly within the accounting interface without additional loan application completion being necessary – is the attractive embedded SME lending model that minimises the application drag.

Category Wise Insights

By Lending Type

Why Does Consumer Lending Lead the Market?

Consumer lending is the largest lending type niche at 44% of total market share in 2025, because P2P platforms have their historical roots in personal loan lending and debt consolidation loans to individual consumers, the credit application segment that first proved the P2P platform to be commercially viable with LendingClub and Prosper as some of the first commercial scale consumer P2P lending platforms in the global platform ecosystem, and the continued existence of a structurally large and well-defined market of personal loans to creditworthy borrowers who could not get bank personal loans at The commercial popularity of consumer P2P lending shows the transparency of the borrower value proposition i.e. P2P personal loan rates of 820 APR versus 1830 APR bank credit cards and 24400 APR payday lending reflect unambiguous borrower savings to credit-worthy individuals whose credit card debt refinancing provides immediate cashflow enhancement, and the simplicity of the investor return profile i.e. consumer loans with 35 years terms and monthly principal and interest payments generate simple yield results and risk management. The most common P2P loan application, and the one with the largest volume of borrowers, is the debt consolidation application where borrowers, with multiple high-rate credit card debts, roll all the debts into a single low-rate P2P personal loan, reflecting the strong financial rationality of the application that creates steady demand among creditworthy borrowers at both ends of an economic cycle.

By End-User

Why Do Individual Borrowers Lead the Market?

Individual borrowers constitute the largest end-user segment with about 48% market share in 2025 including the historical and structural dominance of consumer personal lending in the P2P platform origination mix of the world – with the combination of large addressable borrower population, high credit demand by the underserved consumer segment, and comparatively simple credit evaluation, generating rapid scale-up of origination of consumer P2P platforms decades before the SME and real estate segment. The individual borrower market consists of a heterogeneous group of credit worthy prime and near-prime borrowers who want lower rates than those offered at the bank, thin-file borrowers who have little credit bureau history and need access to credit, self-employed persons whose income profile prevents them to qualify with the bank, and debt burdened consumers who need to consolidate whose repayment ability is evident through cash flow analysis even when bank lending does not consider their credit bureau scores. The fastest growth of the SME financing gap as indicated by the CAGR between 2026 and 2035 is 20.6%, which is indicative of the structural magnitude of the SME financing gap, the commercial validation of the SME P2P lending platforms by the UK market maturity and global growth of Funding Circle, and the increasing accessibility of open banking and accounting software API data which is increasingly contributing to better precision of SME credit assessment and reduced information asymmetry which complicates lending to SMEs comparatively to lending to consumers due to limited SME sector expertise.

By Business Model

Why Does the Marketplace/Platform Model Lead the Market?

The marketplace or platform model, where the P2P platform is the intermediary between borrowers and investors who find and fund loans but the platform gains no loan credit risk on its own balance sheet is the prevailing business model with about 68% market share in 2025, with the capital efficiency advantage of allowing the platform to grow its business without corresponding increase in balance sheet capital, the ability to scale its business with investor capital not limited by platform availability of equity capital, and the original conceptual identity of the pure peer-to-peer marketplace between individual borrowers and lenders, no longer The commercial strengths of the marketplace model such as asset-light growth that facilitates the ability to scale volumes of origination to new heights; investor capital pool flexibility that facilitates the ability to diversify the product of loans; and fee income that are relatively insensitive to credit cycle losses than the balance sheet lender earnings have contributed to the adoption of the model by the largest global P2P platforms such as those of the LendingClub, Prosper, Funding Circle and Mintos whose combined origination volumes comprise the majority of P2P platform lending worldwide. The balance sheet model where the platform takes a substantial%age of originated loans onto its balance sheet secured by equity capital and warehouse debt is gaining momentum in some segments of the market where institutional investor capital has not yet built enough appetite to invest directly in loans, especially in emerging market consumer lending where track records on credit risk assessment and investor trust in platform underwriting quality takes some time to build.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 224.18 billion |

| Projected Market Size in 2035 | USD 1,124.86 billion |

| Market Size in 2025 | USD 187.64 billion |

| CAGR Growth Rate | 17.5% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Lending Type, End-User, Business Model and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

The Asia Pacific peer to peer P2P lending market size is estimated at USD 97.57 billion in 2025 and is projected to reach approximately USD 586.93 billion by 2035, with a CAGR of 19.6% from 2026 to 2035.

Why Did Asia Pacific Dominate the Market in 2025?

Asia Pacific has dominance of about 52%age of the global market share in the year 2025, which depicts the regional dominance of P2P lending volume origination, by the history, which has been symbolized by the phenomenal growth of the P2P lending platforms in China that at its zenith, is the largest P2P lending volume market development landscape in the world, and now, by the systematic and sustained development of the P2P lending platforms in India, Indonesia, Vietnam, South Korea and Australia that together has been the most dynamic market development of The P2P lending market in China, although this time around the regulatory crackdown shut down thousands of non-compliant P2P lending platforms, reorganized around a reduced number of compliant licensed consumer and business lending platforms that act within the current regulatory framework introduced by the 20182020 industry restructuring. The P2P lending market in India Sterilized by the Reserve Bank of India P2P lending Non-Banking Financial Company framework since 2017 is experiencing a rapid growth rate in platforms such as Faircent, LenDenClub, RupeeCircle and i2iFunding who are processing personal loan and SME lending origination to the large population of credit worthy Indian borrowers shunned by traditional bank lending due to documentation requirements, branch availability, or credit bureau thin-file status. The P2P lending sector in Indonesia, governed by the Financial Services Authority through POJK 77/2016 and its subsequent amendments, has grown to have one of the most vibrant P2P lending ecosystems in the Asia Pacific region with more than 100 registered platforms serving the consumer and SME lending requirements of the 275 million people of Indonesia, a high%age of whom are underbanked in terms of their creditworthiness.

Why is North America an Important and Rapidly Growing Market?

It is estimated that the market of North American P2P lenders will have an annual estimate of USD 38.24 billion in 2025 and USD 194.87 billion in 2035 with a CAGR of 17.7. The presence of the United States as the most commercially advanced of all P2P lending markets in the world with the longest operating P2P platform track records LendingClub having facilitated over USD 85 billion total loan commitments since its inception through 2024 the most established institutional investor presence in the P2P lending as an alternative asset class, and the SEC regulatory framework over P2P lending offering investor protection infrastructure to support the mainstream nature of the financial services participation in the U.S. market as compared to most of its counterparts internationally all anchor the market The development of the U.S. P2P market, where personal lending to consumers has given way to the diversification of products on offer, such as auto refinancing, home improvement lending, small business lending, is the commercial maturation of existing platforms and the advent of specialized vertical platforms that are specialized on providing specific credit products, credit models and investors to specific segments of the borrower market. The shift to an industrial bank charter LendingClub has experienced in becoming a banking license model – obtaining an industrial bank charter in 2021 and the shift in technology and credit model sophistication that defines the competitive advantages of platform lending versus traditional banks – is an important structural change that offers LendingClub the benefits of a deposit funding base over pure marketplace competitors whilst still retaining the technological and credit model sophistication which defines the competitive advantages of platform lending against traditional banks.

Why is Europe a Strategically Important Market?

In 2025 European P2P lending market is estimated to have USD 28.46 billion and is estimated to have USD 146.84 billion in 2035 with CAGR of 17.9. Europe is a market of fundamental strategic significance, on which the presence of Zopa (now operating as a digital bank), Funding Circle and rateSetter as the established generation of UK P2P platforms regulated by the FCA and the European Crowdfunding Service Providers Regulation offering the harmonizing licensing framework facilitating pan-European P2P platform operations anchor. The Baltic states, Latvia and Estonia, have built a comparatively large P2P lending market based on their size of population, with Mintos (Latvia) having the largest P2P lending market in Europe in terms of the number of loans listed on their market with investors around the EU financing consumer loans obtained through the partner lenders across a range of European and other international markets. Germany is the largest P2P lending market in Continental Europe – a result of consumer personal lending markets, as well as the large SME lending market to the Mittelstand SME market of Germany whose financing needs are being increasingly met by P2P platforms. The ECSPR regulation of the EU which has done away with the old system where national platforms licensing was required in every country of the EU and has introduced the new system of a single EU wide crowdfunding service provider authorization are establishing regulatory economies of scale in platforms serving more than one country of the EU that will hasten the market development and consolidation of European P2P markets around pan-European platforms capable of deploying investor capital efficiently across multiple national lending markets.

Why is the Middle East & Africa Region an Emerging Market?

The LAMEA region is characterized by the development of an increasing P2P lending market development due to the progressive fintech regulatory development of the Gulf Cooperation Council – with Dubai’s DIFC FinTech Hive regulatory sandbox and the Bahrain central bank fintech regulation framework enabling P2P lending platform operation under the supervision of a well-established regulatory regime in the GCC financial centres – the large population of the unbanked and underbanked in the Middle East creating financial inclusion P2P lending demand, and the extraordinary development of mobile money penetration in Africa creating digital financial infrastructure that P2P lending platforms can build upon for credit delivery without requiring physical branch networks — and Brazil’s rapidly growing fintech sector including P2P lending platforms operating under the Central Bank of Brazil’s fintech regulation framework that has supported the development of a competitive P2P lending market serving Brazil’s large underbanked SME and consumer population.

Top Players in the Market and Their Offerings

- LendingClub Corporation

- Prosper Marketplace Inc.

- Funding Circle Holdings plc

- Zopa Bank Ltd.

- Mintos Marketplace AS

- Faircent (FINCFRIENDS Private Limited)

- Lufax Holding Ltd.

- Yirendai Ltd.

- LenDenClub (Innofin Solutions Pvt. Ltd.)

- Kabbage Inc. (American Express)

- RateSetter (Metro Bank)

- Others

Key Developments

The market has undergone significant developments as industry participants seek to advance AI credit underwriting capabilities, expand institutional investor access products, and respond to the accelerating global demand for alternative credit access across consumer and SME borrower segments.

- In November 2024: LendingClub also announced the creation of its LCX institutional lending platform – which gives institutional investors such as asset managers, insurance companies and bank treasury functions a real-time, direct API connection to LendingClubs consumer and SME loan origination pipeline to select specific loans, apply custom credit filters, and auto-construct portfolios at the rate, and selectivity, institutional portfolio management needs.

- In February 2025: Funding Circle announced the expansion of its FlexiPay SME lending product – UK SMEs are able to access a revolving credit facility of GBP 10,000-GBP 250,000 by launching Funding Circle as their primary working capital management tool alongside term financing of projects – the most significant product development since Funding Circle launched Funding Circles own term loan lending product in 2014.

The Peer to Peer P2P Lending Market is segmented as follows:

By Lending Type

- Consumer Lending (Personal Loans, Debt Consolidation, Medical, Home Improvement)

- Business Lending (SME Working Capital, Invoice Financing, Trade Finance, Equipment)

- Real Estate Lending (Residential, Commercial, Bridge Loans, Development Finance)

- Student Loan Refinancing

- Agricultural Lending

- Other Lending Types (Auto, Green Finance, Microloans)

By End-User

- Individual Borrowers (Employed Individuals, Self-Employed, Gig Economy Workers)

- Small & Medium Enterprises (Micro, Small, Medium Businesses)

- Real Estate Developers

- Agricultural Borrowers

- Other End-Users (Non-Profits, Government-Linked Entities)

By Business Model

- Marketplace/Platform Model (Investor-Funded, Originate-to-Distribute)

- Balance Sheet Model (Platform Retains Loan Exposure)

- Hybrid Model (Mixed Funding and Retention)

- Other Business Models (Notary Model, Guaranteed Return Models)

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Peer to Peer P2P Lending by Segments

- 2.1.2. Peer to Peer P2P Lending by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Peer to Peer P2P Lending Market Attractiveness Analysis, By Lending Type

- 2.2.3. Peer to Peer P2P Lending Market Attractiveness Analysis, By End-User

- 2.2.4. Peer to Peer P2P Lending Market Attractiveness Analysis, By Business Model

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Financial Inclusion Imperative and Credit Access Gap Driving P2P Platform Adoption

- 3.1.2. Small Business Credit Gap and SME Finance Innovation Driving Business P2P Adoption

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Peer to Peer P2P Lending Market – By Lending Type

- 4.1. Lending Type Market Overview, By Lending Type Segment

- 4.1.1. Peer to Peer P2P Lending Market Revenue Share, By Lending Type, 2025 & 2035

- 4.1.2. Consumer Lending (Personal Loans, Debt Consolidation, Medical, Home Improvement)

- 4.1.3. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Business Lending (SME Working Capital, Invoice Financing, Trade Finance, Equipment)

- 4.1.7. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Real Estate Lending (Residential, Commercial, Bridge Loans, Development Finance)

- 4.1.11. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Student Loan Refinancing

- 4.1.15. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Agricultural Lending

- 4.1.19. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Other Lending Types (Auto, Green Finance, Microloans)

- 4.1.23. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Lending Type Market Overview, By Lending Type Segment

- Chapter 5. Peer to Peer P2P Lending Market – By End-User

- 5.1. End-User Market Overview, By End-User Segment

- 5.1.1. Peer to Peer P2P Lending Market Revenue Share, By End-User, 2025 & 2035

- 5.1.2. Individual Borrowers (Employed Individuals, Self-Employed, Gig Economy Workers)

- 5.1.3. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Small & Medium Enterprises (Micro, Small, Medium Businesses)

- 5.1.7. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Real Estate Developers

- 5.1.11. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Agricultural Borrowers

- 5.1.15. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Other End-Users (Non-Profits, Government-Linked Entities)

- 5.1.19. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1. End-User Market Overview, By End-User Segment

- Chapter 6. Peer to Peer P2P Lending Market – By Business Model

- 6.1. Business Model Market Overview, By Business Model Segment

- 6.1.1. Peer to Peer P2P Lending Market Revenue Share, By Business Model, 2025 & 2035

- 6.1.2. Marketplace/Platform Model (Investor-Funded, Originate-to-Distribute)

- 6.1.3. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Balance Sheet Model (Platform Retains Loan Exposure)

- 6.1.7. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Hybrid Model (Mixed Funding and Retention)

- 6.1.11. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Other Business Models (Notary Model, Guaranteed Return Models)

- 6.1.15. Peer to Peer P2P Lending Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Business Model Market Overview, By Business Model Segment

- Chapter 7. Peer to Peer P2P Lending Market – Regional Analysis

- 7.1. Peer to Peer P2P Lending Market Overview, By Region Segment

- 7.1.1. Global Peer to Peer P2P Lending Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global Peer to Peer P2P Lending Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 7.1.3. Global Peer to Peer P2P Lending Market Revenue, By Lending Type, 2026 – 2035

- 7.1.4. Global Peer to Peer P2P Lending Market Revenue, By End-User, 2026 – 2035

- 7.1.5. Global Peer to Peer P2P Lending Market Revenue, By Business Model, 2026 – 2035

- 7.2. North America

- 7.2.1. North America Peer to Peer P2P Lending Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.2.2. North America Peer to Peer P2P Lending Market Revenue, By Lending Type, 2026 – 2035

- 7.2.3. North America Peer to Peer P2P Lending Market Revenue, By End-User, 2026 – 2035

- 7.2.4. North America Peer to Peer P2P Lending Market Revenue, By Business Model, 2026 – 2035

- 7.2.5. U.S. Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.6. Canada Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.7. Mexico Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.8. Rest of North America Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.3. Europe

- 7.3.1. Europe Peer to Peer P2P Lending Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.3.2. Europe Peer to Peer P2P Lending Market Revenue, By Lending Type, 2026 – 2035

- 7.3.3. Europe Peer to Peer P2P Lending Market Revenue, By End-User, 2026 – 2035

- 7.3.4. Europe Peer to Peer P2P Lending Market Revenue, By Business Model, 2026 – 2035

- 7.3.5. Germany Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.6. France Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.7. U.K. Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.8. Russia Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.9. Italy Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.10. Spain Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.11. Netherlands Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.12. Rest of Europe Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific Peer to Peer P2P Lending Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.4.2. Asia Pacific Peer to Peer P2P Lending Market Revenue, By Lending Type, 2026 – 2035

- 7.4.3. Asia Pacific Peer to Peer P2P Lending Market Revenue, By End-User, 2026 – 2035

- 7.4.4. Asia Pacific Peer to Peer P2P Lending Market Revenue, By Business Model, 2026 – 2035

- 7.4.5. China Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.6. Japan Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.7. India Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.8. New Zealand Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.9. Australia Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.10. South Korea Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.11. Taiwan Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.12. Rest of Asia Pacific Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.5. The Middle-East and Africa

- 7.5.1. The Middle-East and Africa Peer to Peer P2P Lending Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.5.2. The Middle-East and Africa Peer to Peer P2P Lending Market Revenue, By Lending Type, 2026 – 2035

- 7.5.3. The Middle-East and Africa Peer to Peer P2P Lending Market Revenue, By End-User, 2026 – 2035

- 7.5.4. The Middle-East and Africa Peer to Peer P2P Lending Market Revenue, By Business Model, 2026 – 2035

- 7.5.5. Saudi Arabia Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.6. UAE Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.7. Egypt Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.8. Kuwait Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.9. South Africa Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.10. Rest of the Middle East & Africa Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.6. Latin America

- 7.6.1. Latin America Peer to Peer P2P Lending Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.6.2. Latin America Peer to Peer P2P Lending Market Revenue, By Lending Type, 2026 – 2035

- 7.6.3. Latin America Peer to Peer P2P Lending Market Revenue, By End-User, 2026 – 2035

- 7.6.4. Latin America Peer to Peer P2P Lending Market Revenue, By Business Model, 2026 – 2035

- 7.6.5. Brazil Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.6. Argentina Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.7. Rest of Latin America Peer to Peer P2P Lending Market Revenue, 2026 – 2035 (USD Billion)

- 7.1. Peer to Peer P2P Lending Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global Peer to Peer P2P Lending Market: Company Market Share, 2025

- 8.2. Global Peer to Peer P2P Lending Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. LendingClub Corporation

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. Prosper Marketplace Inc.

- 9.3. Funding Circle Holdings plc

- 9.4. Zopa Bank Ltd.

- 9.5. Mintos Marketplace AS

- 9.6. Faircent (FINCFRIENDS Private Limited)

- 9.7. Lufax Holding Ltd.

- 9.8. Yirendai Ltd.

- 9.9. LenDenClub (Innofin Solutions Pvt. Ltd.)

- 9.10. Kabbage Inc. (American Express)

- 9.11. RateSetter (Metro Bank)

- 9.12. Others.

- 9.1. LendingClub Corporation

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Custom Market Insights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

List Of Figures

Figures No 1 to 31

List Of Tables

Tables No 1 to 46

Prominent Player

- LendingClub Corporation

- Prosper Marketplace Inc.

- Funding Circle Holdings plc

- Zopa Bank Ltd.

- Mintos Marketplace AS

- Faircent (FINCFRIENDS Private Limited)

- Lufax Holding Ltd.

- Yirendai Ltd.

- LenDenClub (Innofin Solutions Pvt. Ltd.)

- Kabbage Inc. (American Express)

- RateSetter (Metro Bank)

- Others

FAQs

The key players in the market are LendingClub Corporation, Prosper Marketplace Inc., Funding Circle Holdings plc, Zopa Bank Ltd., Mintos Marketplace AS, Faircent (FINCFRIENDS Private Limited), Lufax Holding Ltd., Yirendai Ltd., LenDenClub (Innofin Solutions Pvt. Ltd.), Kabbage Inc. (American Express), RateSetter (Metro Bank), Others.

The most influential determinant of market structure in the P2P lending industry is government regulations, the design of regulatory frameworks directly dictates the rate of market development, product experience of investors and borrowers, and cost structures of platforms, and the conduct rules dictate. The FCA P2P lending regulatory framework of the UK, one of the most sophisticated regulatory systems of P2P lending in the world, and one that places consumer protection of its investors, as well as business-level commercial viability, and market development, the FCA-regulated UK P2P market has grown into one of the most transparent and institutionally credible alternative lending markets in the world despite/because of its comparatively high compliance standards. A case in point is the restructuring of P2P regulation in China where uncompliant platforms were removed and licensed operators remained under the supervision of CBIRC, showing the market-clarifying role of intense regulation that may reduce fraud by investors and contagion caused by platform failure as well as offered a cleaner operating environment to compliant platforms, with the new market providing investors with more confidence than the pre-regulatory environment although admittedly on a smaller scale. The RBI NBFC-P2P framework of India, which offers the most prescriptive specific P2P lending regulatory requirements in the world, including lender aggregate exposure limit, borrower aggregate liability limit, platform fund flow requirements, and credit assessment disclosure standards, establishes comprehensive guardrails that provide investor safeguards without restricting the P2P lending financial inclusion role, and the updates to the 2025 guideline by the RBI address particular practices that had not been properly safeguarded in the original regulatory framework. The ECSPR regulation of the EU, the first supranational harmonized P2P lending regulation in the world that allows cross-border platform operations about 27 member states, shows the potential of regulatory harmonization to speed up the development of markets by lowering cross-border compliance costs that hitherto limited pan-European platform operations, ECSPR providing the regulatory framework through which pan-European markets would consolidate around scale-competitive pan-European platforms within the years that followed the implementation.

The pricing of P2P lending market involves both the borrower interest rates that establish credit demand and the returns of the investors that establish capital supply, with platform economics being in the middle of these two price levels, being the origination and servicing fees income that makes the platform commercially viable. Consumer P2P interest rates and mark-ups to consumers The interest rates on P2P borrowers are determined by risk-based pricing, providing significant borrower savings when compared to credit card rates of 1830%APR and payday lending of 100400% APR to most of the borrower population, which generates the consumer surplus that drives the growth in borrower adoption. The savings in borrowing to the SMEs by way of SME P2P lending at rates of 8-15 APR on term lending to SMEs with good credit profiles and 20-35 APR to working capital lending to riskier SMEs represent the savings to the borrower as compared to the overdraft and credit card business lending options at the bank as well as the increased cost of risk and assessment of lending to SMEs compared to consumer lending. Risk-adjusted returns on P2P platforms of the order of 5 -10% on diversified consumer portfolios and 7 -15% on SME portfolios on established platforms are better than risk-adjusted returns to similar duration government bonds and corporate bonds in low interest rate environments that encourage the allocation of investor capital, but P2P investor returns are competitive in rising rate environments that encourage fixed income options mechanisms that platform operators have to cope with by adjusting the interest rate and product innovation. The major platform revenue model is platform origination fees, which are usually collected upon loan principal by a borrower at the time of disbursement (1-5% of the loan principal), and platform servicing fees, which are usually collected upon outstanding loan balance by the investors on an annual basis (0.5-1.5%), both of which necessitate the platform to realize a sufficient volume of originations in order to amortize the technology infrastructure and regulatory compliance costs that imposes a minimum efficient scale upon any single platform.

According to existing analysis, the market is expected to be USD 1,124.86 billion by 2035 due to the gradual process of global credit markets going progressive and compelling borrowers and investors to increasingly conduct their transactions through digital platforms instead of conventional banking channels, SME P2P lending scaling to mainstream commercial finance as platforms credit models evolve, access to open banking data leading to more available access to the markets, and the dynamic Multi-platform environment of the Southeast Asia creating the dominant global market position of P2P lenders in the geographies with the highest global market position, institutional investor P2P allocation growing as the asset class accumulates the multi-cycle performance track record that institutional investment mandates require, embedded finance integration expanding P2P credit access to borrowers at point of commercial need without platform discovery friction that dramatically improves credit access economics, regulatory framework maturation across Africa, Latin America, and the Middle East creating new regional P2P markets in the world’s most underbanked geographies, and tokenization of P2P loans improving secondary market liquidity and institutional accessibility in ways that structurally increase the investable universe of P2P loans for capital market participants, at a CAGR of 17.5% from 2026 to 2035.

Asia Pacific is expected to maintain the highest revenue share throughout the forecast period, commanding approximately 52% of global market share in 2025, based on the region’s combination of the world’s largest unbanked and underbanked population creating the greatest unmet credit demand, the highest volume of P2P lending origination globally driven by China’s compliant platforms, India’s rapidly growing regulatory-compliant P2P market, and Southeast Asia’s dynamic multi-country P2P ecosystem, the region’s mobile-first digital financial services adoption enabling P2P platform reach without physical banking infrastructure, the strong government and regulatory support for fintech-enabled financial inclusion in India, Indonesia, Singapore, and progressively across the region creating enabling policy environments for P2P platform growth, and the extraordinary scale of Asia Pacific’s SME sector — representing the world’s largest concentration of underfinanced SMEs — whose financing gap provides the most significant addressable business lending opportunity for P2P platforms globally.

Asia Pacific will sustain the largest share of the revenue globally over the forecast period, owning nearly half of the global market share in 2025, based on the combination of the largest unbanked and underbanked population on Earth, the highest source of P2P lending origination in the world with the aid of China compliant platforms, the fastest growing regulatory-compliant P2P market in India, and the dynamic multi-country P2P ecosystem in Southeast Asia, the mobile-first digital financial service adoption of the Asian market providing P2P platforms to reach unaddressed credit demand creating the ideal conditions for P2P platform adoption at unprecedented scale.

The Global Peer to Peer P2P Lending Market is expected to experience a significant growth rate as the World Bank estimates that there are about 1.4 billion unbanked adults in the world that make the P2P platforms the demand side of the financial inclusion infrastructure, the IFC documenting an annual USD 5.2 trillion SME financing gap in the formal financial system credit supply creating the largest addressable business lending opportunity in P2P platforms, LendingClub published research that a 15-20% reduction in charge-off rates through the use of AI-enhanced underwriting while extending credit approval to 20–30% more applicants validating the dual financial inclusion and risk management benefits of AI credit models, India’s Account Aggregator framework enabling P2P platforms to access borrower financial data through API connections creating regulatory infrastructure supporting alternative data credit assessment at scale, the EU’s European Crowdfunding Service Providers Regulation providing harmonized EU-wide P2P platform licensing eliminating the multi-national registration barrier to pan-European market development, LendingClub’s LCX institutional platform attracting USD 2.8 billion in committed institutional capital within 90 days demonstrating the appetite for direct loan selection access that institutional portfolio management demands, RBI’s revised P2P guidelines strengthening investor protection while maintaining regulatory support for P2P lending as financial inclusion infrastructure, and the McKinsey Global Institute quantifying that extending credit access to the underbanked through digital financial services could add USD 3.7 trillion to emerging market GDP providing authoritative economic justification for P2P platform investment and regulatory support.